Mortgage Calculator How Much House Can You Afford?

Table Of Content

Budget 1% to 4% of your home’s value each year for home maintenance. You might not spend this amount each year, but you’ll spend it eventually. By refinancing an existing loan, the total finance charges incurred may be higher over the life of the loan. This formula will come in handy when determining how much home you can afford. Annual income is the amount of documented income you earn each year.

Other Financial Considerations

Because building equity can grow your net worth and give you better borrowing options, you may be better off if you begin that process sooner rather than later.

Figure out 25% of your take-home pay.

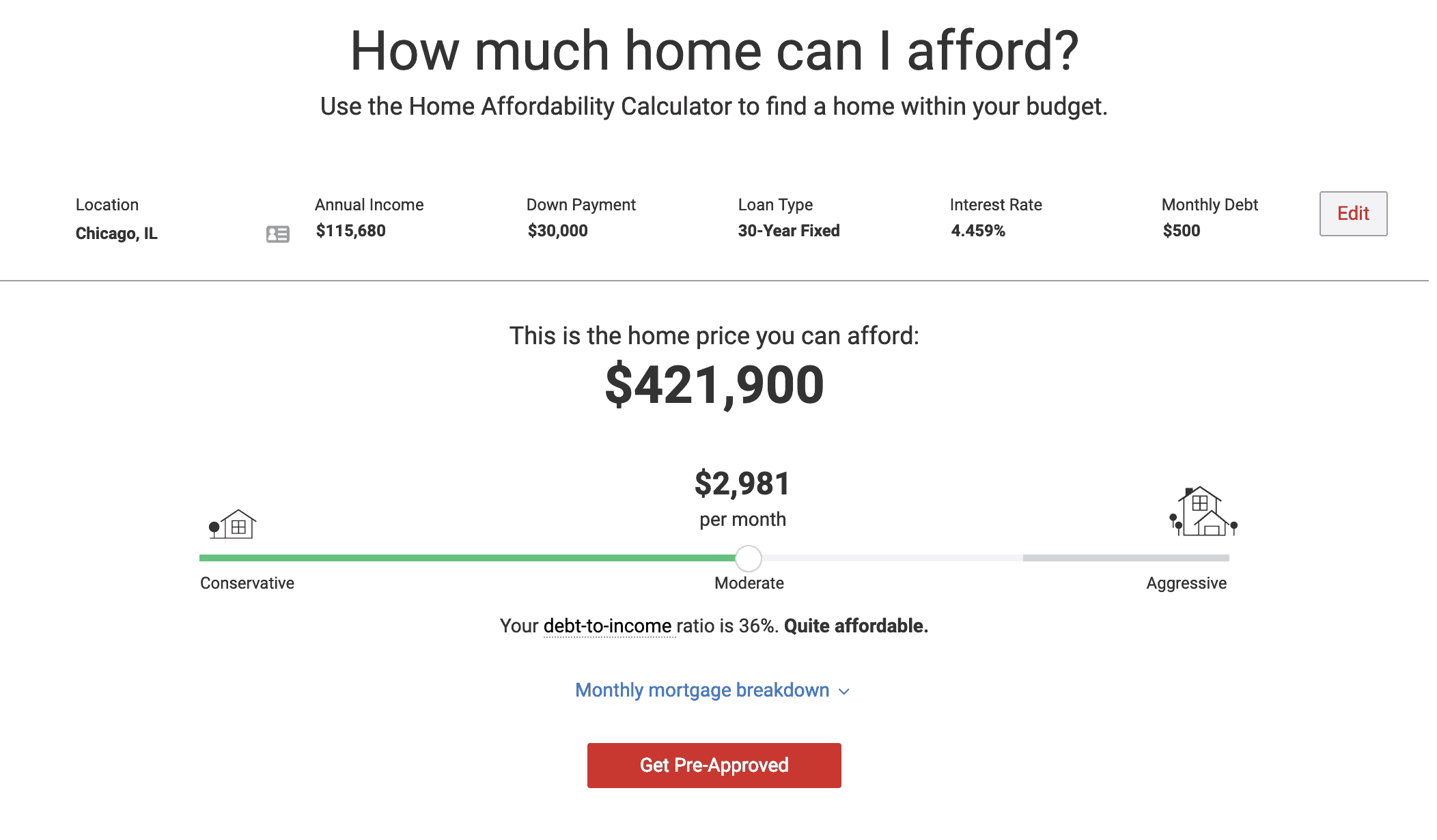

→ The 28 is a recommended DTI ratio for your monthly mortgage payment compared to your gross monthly income. The Loan Estimate (LE) shows your total mortgage costs — including the down payment, closing costs, monthly payments, and interest paid over the life of the loan. When lenders assess whether or not you can afford a mortgage loan, they’ll compare your estimated PITI with your gross monthly income (income before taxes and deductions). The amount you'll need to close your loan includes your down payment, closing costs, and prepaid escrow amounts for property taxes and insurance.

What is the difference between APR vs interest rate?

Most home loans require a 20% down payment, but Federal Housing Administration (FHA) loans only require a minimum of 3.5%. This type of loan opens the door for many potential homeowners that do not have the savings for a substantial down payment. However, this loan typically requires private mortgage insurance (PMI) which should be added into your monthly expenditures.

However, a shorter mortgage term requires higher monthly payments since the total amount repaid is spread across a shorter length of time. Estimate your monthly payments, closing costs, APR and mortgage interest rate today. Fixed-rate loans have the same interest rate for the entire duration of the loan.

Property taxes in California are a relative bargain compared to the rest of the nation. With limits in place enforced by Proposition 13, generally property taxes cannot exceed 1% of a property’s market value. With those rules, California’s effective property tax rate is just 0.71%. On the local and county level, additional taxes can be levied if you live in a special district that’s financing an improvement or other local concern. Mortgage pre-approval is a statement from a lender who’s thoroughly reviewed your finances and decided to offer you a home loan up to a certain amount. Pre-approval is a smart step to take before making an offer on a home, because it will give you a clear idea of how much money you can borrow to pay for a house.

If you’re considering a property on the coast, you’ll want to take a look at the National Flood Insurance Program (NFIP) to help protect yourself from flood losses. If you are looking to buy a house that requires a mortgage above these caps, you’ll need to take out something called a jumbo loan. You can still use the calculator to get a sense of what you might be able to afford, though it will be less accurate. Short-term mortgages offer less protection against changing interest rates because you need to renew them more frequently. Long-term mortgages typically have higher rates but offer more protection against rising interest rates. Penalties for breaking a long-term mortgage can be higher for this type of term.

Use this tool to calculate the maximum monthly mortgage payment you'd qualify for and how much home you could afford. Please visit our FHA Loan Calculator to get more in-depth information regarding FHA loans, or to calculate estimated monthly payments on FHA loans. There are several ways you can make buying a home more affordable. Some of the best include increasing your income, decreasing your monthly payment by making a bigger down payment, and moving to a more affordable neighborhood. Down payment & closing costsNerdWallet's ratings are determined by our editorial team. The scoring formula takes into account the type of card being reviewed (such as cash back, travel or balance transfer) and the card's rates, fees, rewards and other features.

Mortgage Prequalification Calculator – Forbes Advisor - Forbes

Mortgage Prequalification Calculator – Forbes Advisor.

Posted: Mon, 21 Aug 2023 07:00:00 GMT [source]

They are basic debt-to-income ratios (DTI), albeit slightly different and explained below. For more information about or to do calculations involving debt-to-income ratios, please visit the Debt-to-Income (DTI) Ratio Calculator. This is a separate calculator used to estimate house affordability based on monthly allocations of a fixed amount for housing costs. On average, closing costs are about 3–4% of the purchase price of your home—and you need to be able to pay for them with cash.1 So start saving!

Key factors in calculating affordability are 1) your monthly income; 2) cash reserves to cover your down payment and closing costs; 3) your monthly expenses; 4) your credit profile. A good affordability rule of thumb is to have three months of payments, including your housing payment and other monthly debts, in reserve. This will allow you to cover your mortgage payment in case of an unexpected event.

You’ll also want to pay attention to how much debt you have, the size of the home loan you want, the amount of money you need to put down, and more. These factors can all influence how much home you can reasonably afford. The exact amount you’ll qualify for will depend on your finances and vary from lender to lender. The best way to determine how much mortgage you can qualify for is to start the mortgage application process.

How much of a lump sum payment you can make without penalty depends on the original mortgage principal amount. Make a mortgage payment, get info on your escrow, submit an insurance claim, request a payoff quote or sign in to your account. Go to Chase home equity services to manage your home equity account. Learn how much income you’ll need to buy a house and what lenders consider when reviewing applications. Evaluate your full financial situation, your ability to pay off a mortgage and where you need to save for other expenditures. Once you’ve done all that, it’s time to go after that perfect home.

Sky high mortgage rates have pushed many hopeful buyers out of the market, slowing homebuying demand and putting downward pressure on home prices. The current supply of homes is also historically low, which will likely push prices up. Mortgage lenders are required to assess your ability to repay the amount you want to borrow.

Apply online for expert recommendations with real interest rates and payments. This video shows you how your mortgage payment should fit comfortably into your lifestyle. Zillow's mortgage calculator gives you the opportunity to customize your mortgage details while making assumptions for fields you may not know quite yet. These autofill elements make the home loan calculator easy to use and can be updated at any point.

Borrowers must pay for mortgage insurance in order to protect lenders from losses in instances of defaults on loans. The insurance allows lenders to offer FHA loans at lower interest rates than usual with more flexible requirements, such as lower down payment as a percentage of the purchase price. Lenders will also look at your debt-to-income ratio, or DTI, to get a clear picture of how risky it is to loan you money. Simply put, the higher your debt-to-income ratio, the more the lender will doubt your ability to pay the loan back.

USDA loans require no down payment, and there is no limit on the purchase price. However, these loans are geared toward buyers who fit the low- or moderate-income classification, and the home you buy must be within a USDA-approved rural area. Let’s say you earn $100,000 each year, which is $8,333 per month. By using the 28 percent rule, your mortgage payments should add up to no more than 28 percent of $8,333, or $2,333 per month. That’s a big deal, because mortgages backed by the Department of Veterans Affairs typically don’t require a down payment.

Comments

Post a Comment